March 13 2026

Trusted Intelligence in Finance: What We Learned from Our Financial Services Roundtable

Digital transformation is accelerating rapidly across financial services. Artificial intelligence, open finance and real-time data are changing how institutions operate and how customers interact with money.

But one challenge sits at the centre of all of this change: trust.

At our recent Mediaworks Finance Roundtable, senior leaders from across banking, fintech and digital strategy came together to explore what it takes to build trusted intelligence in finance. The session combined expert discussion with live audience polling, offering a unique view into how organisations are currently navigating this shift.

What emerged was a clear message. Technology capability is advancing quickly. Customer confidence is not keeping pace.

Below are four key insights from the discussion.

1. AI Is Operational, but Explainability Is Still Missing

Artificial intelligence is now embedded across financial services, influencing everything from credit scoring and fraud detection to underwriting and customer support.

But the roundtable discussion revealed a significant gap between AI capability and customer understanding.

Research presented during the session showed that 72% of consumers are comfortable with AI in finance only if decisions remain explainable. Yet complaints across banking products continue to rise, highlighting growing friction between automated decision-making and customer perception.

When we asked the audience:

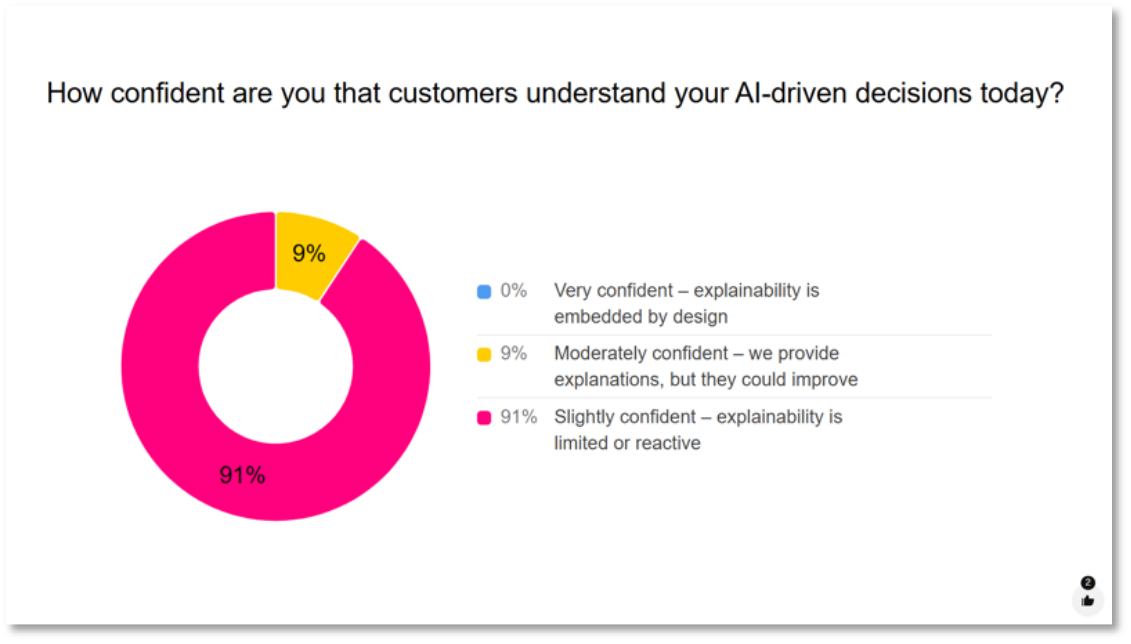

How confident are you that customers understand your AI-driven decisions today? The results were striking:

The results were striking:

91% said explainability is limited or reactive

9% said they were moderately confident

No organisations reported that explainability was embedded by design.

The conclusion from the panel was clear. Most institutions have invested heavily in model performance, but far less in the experience layer surrounding automated decisions.

As one of the panellists observed, organisations often deliver:

statistically correct decisions

compliant processes

but increasing complaints due to opaque outcomes.

In a Consumer Duty environment, that is no longer sustainable. Explainability must be treated as a design requirement, not simply a compliance obligation.

2. Visibility Does Not Mean Customers Understand You

The second theme explored a growing disconnect in digital performance measurement.

Financial services organisations have become highly sophisticated in tracking digital visibility. But very few measure whether customers actually understand the information they are presented with.

Industry research cited during the session showed that 57% of customers say clear online information is the single biggest factor when choosing a financial provider. Despite this, most organisations still measure success through metrics such as:

traffic

rankings

impressions.

When we asked attendees:

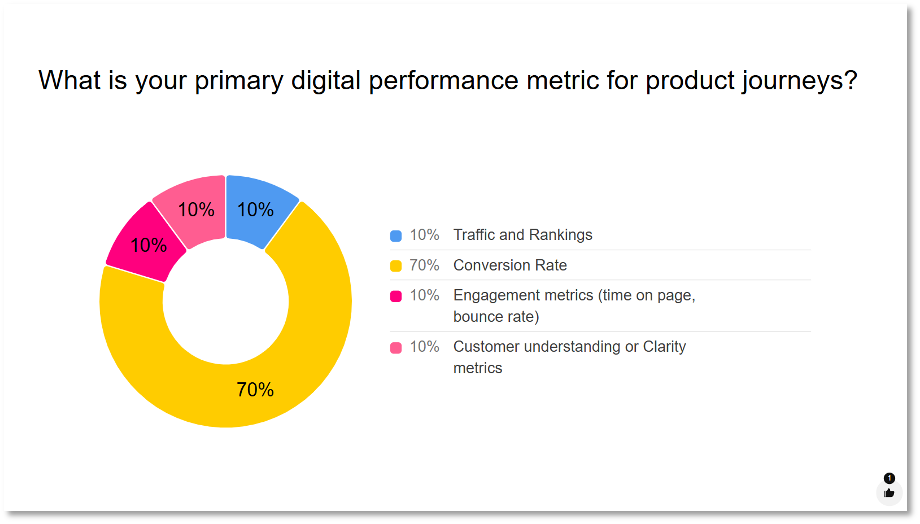

What is your primary digital performance metric for product journeys?

The results showed:

The results showed:

70% prioritise conversion rate

10% measure traffic and rankings

10% measure engagement

Only 10% measure customer understanding or clarity metrics.

The panel argued that this is a major blind spot.

Many financial institutions have strong brand awareness and strong digital reach. But customers often struggle to understand product eligibility, pricing structures or the next step in a journey.

As one of the speakers summarised it:

Awareness is often strong. Comprehension is weak.

In a world shaped by Consumer Duty and rising customer expectations, digital visibility must evolve into digital comprehension.

3. FinTech Has Permanently Reset Trust Expectations

FinTech has fundamentally changed what customers expect from financial services.

Features such as:

real-time balances

instant notifications

transparent fees

simple onboarding

have become the new baseline for customer experience.

Today, 93% of UK adults use at least one form of remote banking, and digital-only banks are rapidly gaining credibility. In fact, 46% of UK business leaders now trust digital-only banks as much as traditional institutions.

The roundtable explored where organisations believe they are most exposed to trust erosion.

The audience poll asked:

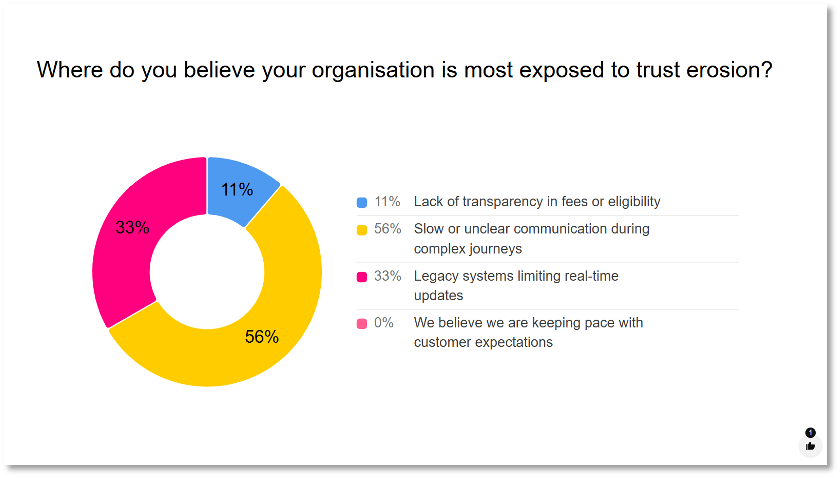

Where do you believe your organisation is most exposed to trust erosion?

The results revealed a clear theme:

The results revealed a clear theme:

56% said slow or unclear communication during complex journeys

33% said legacy systems limiting real-time updates

11% said lack of transparency in fees or eligibility

No respondents believed their organisation was fully keeping pace with expectations.

The panel agreed that the biggest driver of trust is not brand reputation, but experience design.

Customers want:

progress visibility

predictable communication

clear timeframes

transparent outcomes.

When these signals are missing, uncertainty increases and trust declines.

4. Customers Are Open to Data Sharing, but Only When Trust Is Visible

The final theme explored the rapid growth of open finance.

Open Banking API calls in the UK reached 24 billion in 2025, up 37% year-on-year, demonstrating the accelerating adoption of data-driven financial services.

But the panel made an important point: open banking is not really about banking.

As one speaker explained:

The big uptick in open banking isn’t about banking. It’s about trust.

Customers are increasingly willing to share financial data with third parties if they see clear value in doing so.

During the session we asked:

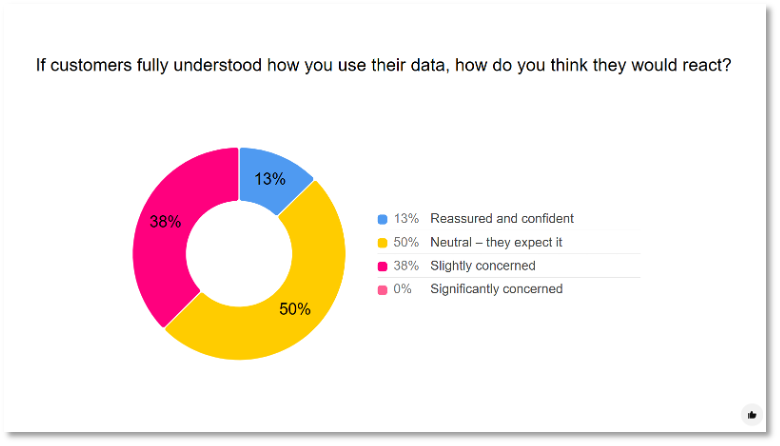

If customers fully understood how you use their data, how would they react?

The audience responses were revealing:

The audience responses were revealing:

50% said customers would be neutral – they expect it

38% said customers would be slightly concerned

13% said customers would be significantly concerned

Only a small minority believed customers would feel fully reassured.

This suggests that while customers are open to data-driven services, organisations must make governance and value exchange far more transparent.

Customers will share data when they:

trust the organisation

understand how their data will be used

see tangible benefits from doing so.

The Strategic Shift: From Automation to Responsible Intelligence

Across all four discussions, a consistent pattern emerged.

Financial services organisations are already partway through a major transformation. But the next stage of that transformation will not be defined by technology alone.

It will be defined by responsible intelligence.

That means shifting:

from automation to explainable intelligence

from reach metrics to understanding metrics

from brand-led trust to experience-led trust.

Ultimately, the organisations that succeed will be those that design digital systems that customers can both use and understand.